Updated August 22, 2025 by Drew

In this post:

Quick Verdict

Despite a recent Qantas points devaluation and a higher forex fee, the ANZ Frequent Flyer Black remains one of Australia’s top-tier Qantas cards in 2025, thanks to its massive 130,000-point sign-up bonus and solid domestic earn rate. It’s a clear winner for Qantas loyalists who can meet the spend for the bonus and use the lounge passes, easily offsetting the $425 annual fee in the first year. However, the new 3.5% foreign transaction fee makes it a poor choice for overseas spending.

We’ve covered the ANZ Frequent Flyer Black card years ago on Points Brotherhood, and it’s consistently been a powerhouse for Qantas points earners. But since our last full review, the landscape has shifted significantly. With a major Qantas devaluation now a reality, a higher foreign transaction fee, and a longer churn period, it’s time for a fresh look. Is this card’s massive sign-up bonus still enough to justify its place in your wallet?

In this 2025 review, I’ll break down whether the hefty annual fee is justified, especially when compared to recently devalued rivals like the CommBank Ultimate Awards card. As someone who actively churns cards for maximum value, here’s my detailed take.

The Big-Ticket Benefits: What Do You Actually Get?

This card’s appeal boils down to high Qantas points earn and travel perks. You’ll earn a solid 1 Qantas Point per $1 on eligible everyday spend, boosted to 2 points per $1 on Qantas products and services. The two complimentary Qantas Club lounge passes each year are perfect for domestic trips, and the included international travel insurance provides peace of mind, making it a strong all-rounder for flyers chasing rewards.

What’s Changed Since Our Last Review?

It’s been a tough year for points collectors. Here’s a summary of the key changes:

- Higher Forex Fee: ANZ hiked the overseas transaction fee from 3% to a painful 3.5% effective May 2, 2025.

- Longer Churn Period: The eligibility period to re-apply for a bonus was extended from 12 to 24 months in May 2025, making it harder to churn this card for repeat bonuses.

- Qantas Devaluation: The biggest hit is Qantas’s own August 2025 devaluation, which increased the points needed for Classic Flight Rewards by up to 20% on some routes.

While this stings, ANZ’s direct Qantas earn still holds its ground, especially when you see that CommBank gutted its Ultimate Awards card in October, leaving Velocity as its only major airline transfer partner.

How to Apply & Get the Bonus

You can apply directly on the anz.com.au website. Before you do, check the eligibility:

- You must be 18+ with good credit.

- An Australian/New Zealand resident or hold a visa with more than 12 months remaining.

- You can’t have held an ANZ Frequent Flyer or ANZ Rewards card in the last 24 months to get the bonus points.

The current offer is a beast: get 90,000 bonus Qantas Points and a $200 statement credit when you spend $5,000 in the first 3 months. Plus, an extra 40,000 bonus points if you keep the card for over 12 months.

Pros and Cons: The ANZ Frequent Flyer Black

Pros

- Huge Sign-Up Bonus: Up to 130,000 bonus Qantas Points + $200 back is one of the best offers on the market.

- Lounge Access: Two Qantas Club lounge passes per year are genuinely useful (worth ~$100 each).

- Complimentary Insurance: Decent international and domestic travel insurance, plus purchase protection.

- Uncapped Points: While the earn rate drops, your total points earning is uncapped.

Cons

- High Annual Fee: The $425 annual fee is significant if you don’t use the benefits.

- Tiered Earning Rate: The earn rate halves to 0.5 points per $1 after you spend $7,500 in a statement period.

- High Forex Fee: At 3.5%, this card is a poor choice for spending overseas.

- Long Churn Lockout: The 24-month wait to get another bonus hurts its churn value.

- High Interest Rate: As always, avoid interest charges. The 20.99% p.a. rate on purchases will wipe out any points value.

Earning Rates and Points

Points are earned directly into your Qantas account and never expire as long as you earn or redeem at least one point every 18 months.

| Category | Qantas Points per $1 | Caps/Exclusions |

|---|---|---|

| Eligible Purchases (up to $7.5k/month) | 1 | Drops to 0.5 after $7.5k |

| Qantas Products/Services | +1 bonus (total 2) | QF flights, FF/Club fees; excl. Jetstar |

Redeeming Points: What Are They Worth?

The best value comes from redeeming points for flights—specifically Business and First Class seats. After the August 2025 devaluation, you’re looking at a value of 1-2 cents per point for Economy, but this can jump to 4-8 cents per point (or even higher) for premium cabin redemptions. Avoid using points on toasters and gift cards; it’s a terrible waste.

Comparison: ANZ Frequent Flyer Black vs. CommBank Ultimate Awards

With CommBank devaluing its transfer partners in October 2025, this comparison has become much simpler for Qantas loyalists.

| Feature | ANZ FF Black | CommBank Ultimate Awards (Qantas Opt-In) |

|---|---|---|

| Annual Fee | $425 | $420 ($35/month, waivable) |

| Bonus | Up to 130k Qantas | Up to 100k Awards (70k Qantas) |

| Earn per $1 (Intl) | 1 (3.5% forex) | 1.2 (no forex) |

| Caps | 0.5 after $7.5k/month | 0.2 after $10k/month |

| Lounges | 2 Qantas Club | 2 Mastercard Travel Pass |

| Transfers/Flexibility | Direct Qantas | Velocity only post-Oct |

The verdict here is clear: The ANZ card is the winner for maximising your Qantas points balance, especially with the huge sign-up bonus. The CommBank card is now only superior for those who spend a lot overseas (due to no forex fees) and are happy earning Velocity points.

Alternatives to the ANZ Frequent Flyer Black

While the ANZ FF Black is a strong contender, it’s not the only game in town. Depending on your spending habits and loyalty, these alternatives might be a better fit. As we’ve analyzed before on this blog, the right card for you often comes down to the finer details.

- CommBank Ultimate Awards: A direct competitor we reviewed previously. It wins on having no foreign transaction fees, but its value took a big hit after it lost most of its airline transfer partners. You can read our full review here.

- St George Amplify Signature: A fantastic choice for flexibility. It allows transfers to both Velocity and international partners like KrisFlyer, with uncapped points earning. Check out our St George Amplify review for more details.

- Amex Qantas Ultimate: Often comes with a strong sign-up bonus and boasts a higher ongoing earn rate of 1.25 points per dollar, making it a powerful earner for dedicated Qantas flyers.

- Virgin Money Velocity High Flyer: The go-to option if you’re on Team Velocity instead of Team Qantas.

- Fee-Free Options: If you just want a good travel card without the points complexity, cards from ING or Up Bank offer no foreign transaction fees and are great for overseas spending.

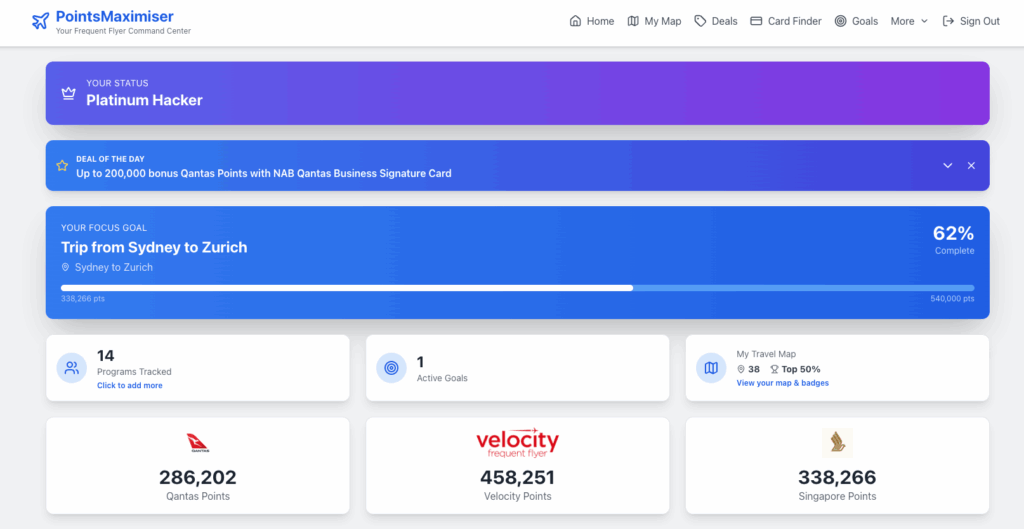

Maximize Your Points with Points Maximiser

Tracking your ANZ Qantas points alongside others from different cards? Points Maximiser (pointsmaximiser.com.au) is a tool we’re developing that aggregates all your balances using AI, helping you spot deals and expiries—which is key in a post-devaluation world.

Key features include:

- Track Everything: See your Qantas, Velocity, and other bank point balances in one place.

- AI Advisor: Get strategies like “Redeem your Qantas points before the devaluation hits.”

- Card Finder: Scan for bonuses for all the major banks and Amex

- Goals & Estimator: Set trip targets, estimate points needed, and get pro tips.

- Deals Feed: AI-powered alerts for earning/spending, even for non-enrolled programs.

- My Map: Fun tracker for visited countries, with wishlists and sharing.

Sign up for the waitlist to get early access—it’s beta but already helps avoid points waste.

Verdict: Is the ANZ Frequent Flyer Black Worth It?

Yes, but only if you are laser-focused on Qantas and can easily meet the $5,000 spend requirement for the bonus. The value proposition is simple: the 130,000 bonus points are worth at least $1,300 in economy flights, which smashes the $425 annual fee in the first year.

Who is this card for?

- First-time premium card applicants looking for a massive upfront bonus.

- Qantas loyalists who can benefit from the lounge passes and bonus earn rate on Qantas spend.

Who should avoid it?

- Anyone who spends a lot of money overseas (that 3.5% fee will hurt).

- High-spenders putting more than $7,500 a month on the card.

My strategy? I applied for the bonus, will max out its benefits for the year, and then re-evaluate before the second annual fee hits. It’s a fantastic card for a first-year value boost, especially before any potential RBA changes further water down the points game.

What do you think—still worth the fee? Share your take in the comments below!