The Dress That Made Me Build a Calculator

I spend a lot on foreign transactions. More than most — travel four or five times a year, ski seasons where I help cover the family, cruises, subscriptions billed in USD, flights booked direct with overseas airlines. I’ve always had a rough sense of which card was best for overseas spending. But it was a dress in Singapore that made me realise rough sense wasn’t good enough.

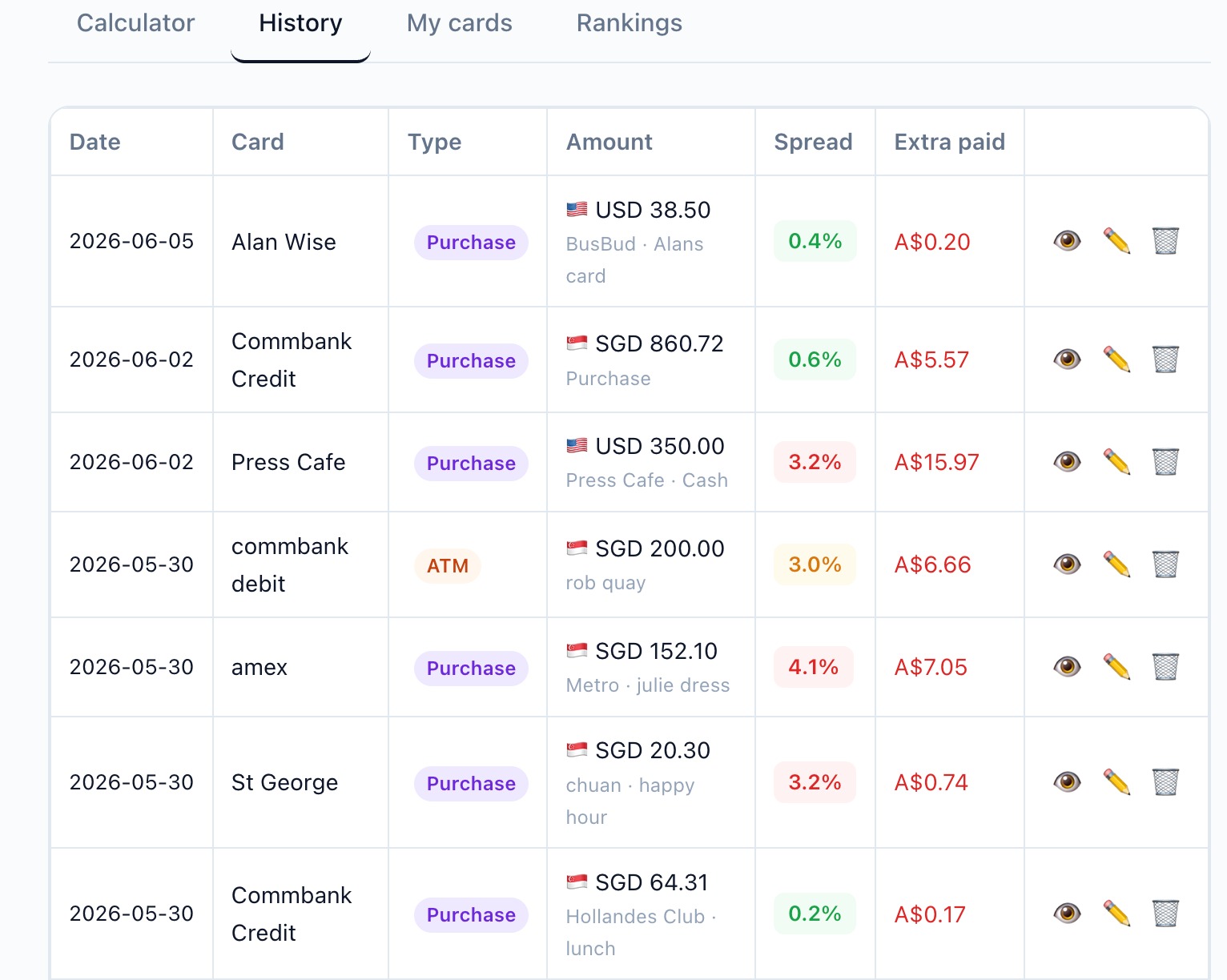

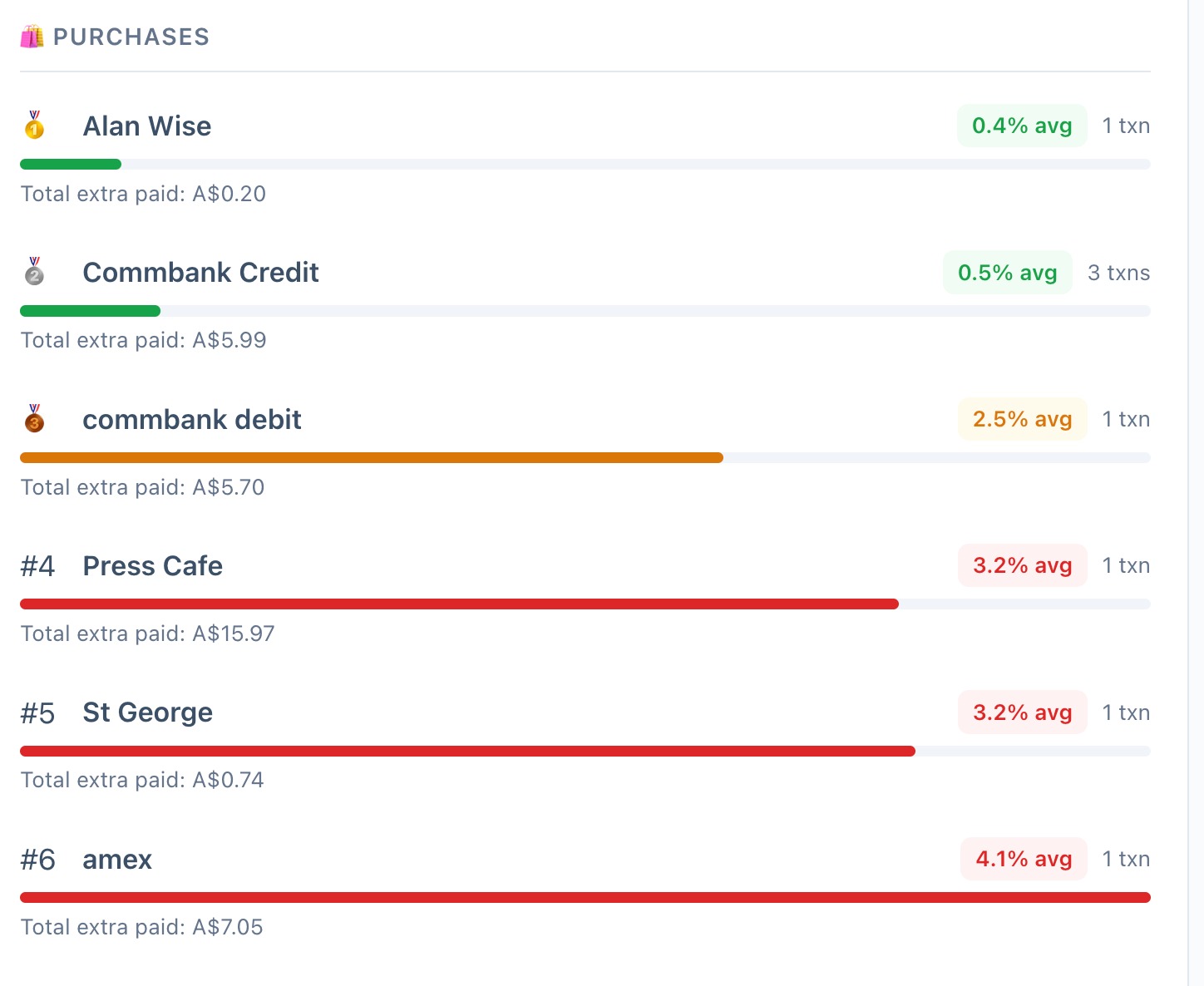

Julie found it at Metro in Orchard Road. SGD 152 — about A$170. She pulled out the Amex, which is perfectly reasonable: great card, earns good points, feels right for a shopping moment. What neither of us was tracking in that moment was the exchange rate. I entered the transaction into the calculator afterwards. The spread was 4.1%. She’d paid an extra A$7.05 on a $170 dress.

That’s not a disaster. But when I showed her the number — and explained that every Amex purchase overseas was doing the same thing — I watched her rethink which card to reach for. That one moment, made visible, was the whole point of the tool.

I know my cards. I just couldn’t prove it.

My daily card overseas is the CommBank Ultimate Awards Credit Card. I like it for reasons that go well beyond the exchange rate: no international transaction fees, up to 44 interest-free days, complimentary travel insurance (which I have actually used — I got knocked out cold on the slopes in Switzerland and it worked exactly as it should), two free airport lounge passes per year via Mastercard Travel Pass, strong fraud protection (my card was compromised in Argentina once — CommBank had it sorted before I’d finished my coffee), and it sits right inside the CommBank app I already use for everything. Convenience matters when you’re moving between countries.

The FX performance reflects the card: no international transaction fee on purchases, which is why it averages 0.5% in the calculator. My CommBank World Debit, which I use for ATM withdrawals, runs closer to 2.5% — different fee structure, different use case. The Amex, which I use less overseas now, sits at 4.1%.

One thing worth knowing: the Ultimate Awards card carries a $35 monthly fee, waived if you spend $4,000 per statement period — or in my case, covered by a Wealth Package arrangement. It is not free for everyone, so check the full picture before assuming the same numbers apply to you.

None of that surprised me in direction. The numbers just made it real.

My friend Alan and his Wise card

Alan has been telling me Wise is the cheapest card for overseas spending for years. He’s right. His Wise card sits at 0.4% — near the mid-market rate, minimal margin, hard to beat on pure FX cost.

For Alan’s style of travel, it’s the right card. For mine, there’s a trade-off worth making: CommBank credit at 0.5% is close enough to Wise that the gap on any normal purchase is cents. And CommBank credit gets me into airport lounges via Priority Pass, which I use regularly — you can check exactly which cards get you into which lounges at the Lounge Finder. Alan gets the cheaper rate and queues at the gate. Both choices are defensible. The point is knowing what you’re trading.

What does it actually cost you in a year?

FX fees aren’t just a travel problem. Subscriptions billed in USD, software tools, flights booked direct with overseas airlines, a cruise paid in USD — all of it touches a foreign exchange rate. If your total overseas spend across travel and subscriptions is $30,000 a year, a 3% card costs you $900. A 0.5% card costs you $150. The difference is real money, and it’s invisible unless you measure it.

💸 What is your card costing you?

Checking the rate before I hand over the cash

There's a currency exchange at a café in Fairlight that I use when I need physical cash before a trip. I needed USD for an upcoming Mekong River trip — ATMs can be unreliable in that part of the world, so a float of physical dollars is just sensible planning. They quoted me a rate, I opened the app on my phone, entered the numbers, and it came back at 3.2%.

For cash, that's actually reasonable — airport kiosks typically run 8–12%. I knew that instinctively, but now I had the number in front of me. I exchanged there and went on my way. The tool confirmed what I suspected; it didn't change the decision, but it grounded it. That's most of what it does.

I built it for me — and then for everyone else

I'd done this exercise once before with a spreadsheet. It worked once, produced some useful numbers, and I never opened it again. The friction killed it: find the file, find the tab, look up the exchange rate somewhere else, remember which column is which. Fifteen minutes to do something that should take fifteen seconds.

The calculator solves that. It's always at the same URL. It fetches the live mid-market rate automatically. You enter a transaction in seconds. The history builds. Over time — a trip, a year — you get a real picture of what your cards are actually costing you, not a theory.

Add your own cards, track your own transactions, see your own rankings. The data stays on your device — nothing is sent anywhere. If you travel with an eSIM (I use Airalo — it's the one thing I'd never travel without now), you can be tracking your first transaction before you've cleared customs.

Frequently Asked Questions

The CommBank Ultimate Awards Credit Card charges no international transaction fee on purchases — that is the main reason the spread sits at 0.5% in the calculator. It runs on the Mastercard network, which uses a rate very close to the mid-market rate, and with no fee layered on top the total cost stays low. The CommBank World Debit is a different product with a different fee structure — useful for ATM withdrawals but a different FX story. The Ultimate Awards card also carries a $35 monthly fee, waived if you spend $4,000 per statement period. See the full CommBank Ultimate Awards review on Points Brotherhood for the detail.

If your bank card is genuinely low-spread — 0.5% or under — the practical difference against Wise on a normal transaction is cents. Where Wise pulls ahead is on large amounts, ATM withdrawals, or if your bank card has an additional flat fee. The bigger question is what else your bank card does: lounge access, fraud protection, points, interest-free days. If those matter to you, the marginal FX difference against a good bank card often doesn't justify the switch. Use the calculator on your own transactions and decide based on actual numbers rather than assumptions.

Yes. Any service or purchase billed in a foreign currency goes through the same FX spread as an overseas transaction. It is easy to forget because some of these charges happen automatically in the background, but they add up across a year. You can check them the same way as any travel purchase: enter the foreign amount and the AUD you were charged, and the calculator will show you the spread.

Always local currency. When a terminal or ATM offers to charge you in Australian dollars — called Dynamic Currency Conversion — they apply their own exchange rate on top of your bank's. You end up paying two margins instead of one. Select the local currency option every time and let your card do the conversion. The only exception would be if you already know your card has a particularly bad rate and the merchant's conversion somehow beats it — extremely rare, and you'd need to know your card's spread to judge it.

Not always. Airport kiosks are typically 8–12% above mid-market — genuinely poor value. But a decent local exchange bureau can come in at 3–3.5%, which is comparable to or better than using an ATM abroad with a debit card that has a flat withdrawal fee. The calculator handles cash exchanges too: enter the foreign amount you received and the Australian dollars you paid, and it calculates the effective spread. That number tells you whether the rate was worth taking.

The Points Brotherhood Lounge Finder covers 196 lounges across 34 airports, searchable by airport and card. It shows which Australian cards — CommBank, Amex, ANZ, and others — provide access at each airport, including via Priority Pass. Used alongside the FX calculator, it gives you a full picture of what each card costs and what it gets you.